If you’re looking to lease a commercial vehicle—such as a van, pickup, or fleet of vehicles for your business—you’ll need to pass a credit check as part of the application process for a commercial vehicle contract.

Credit checks are a standard requirement for any form of business vehicle finance. Lenders use them to assess the financial reliability of your business and determine whether you’re suitable for a leasing agreement. The outcome not only affects approval but also influences the terms you’re offered, including monthly payments, initial deposit, and contract structure.

For companies offering commercial vehicle contracts, credit assessments help ensure agreements are responsibly structured and sustainable for both parties.

Why Is A Credit Check Required For Commercial Vehicle Leasing?

A credit check allows a finance provider to review your business’s financial background and repayment behaviour. This typically includes:

- Outstanding business credit and loans

- Repayment history on existing agreements

- Any missed or late payments

- Public records such as CCJs or insolvency events (if applicable)

- Length and stability of your trading history

The goal is to assess risk. A business with a strong credit profile is generally seen as lower risk, which can improve the likelihood of approval and access to more competitive leasing terms.

For commercial vehicle contracts, lenders are also evaluating the stability of your business operations, not just personal finances (where applicable), especially for sole traders and small businesses.

How Credit Checks Work In Vehicle Leasing

When you apply for a commercial vehicle lease, the provider will carry out either a soft or hard credit check, depending on the stage of the application.

Soft Credit Check

A soft credit check is typically used for initial eligibility assessments. It:

- Does not affect your credit score

- Is not visible to other lenders

- Provides a high-level view of your credit profile

This type of check is useful for understanding your likelihood of approval before submitting a full application.

Hard Credit Check

A hard credit check is carried out when you formally apply for a commercial vehicle contract. It:

- Leaves a record on your credit file

- May have a temporary impact on your credit score

- Is visible to other lenders

Multiple hard searches in a short period may signal increased borrowing activity, so it’s advisable to space out applications where possible.

What Do Lenders Look For?

When assessing applications for commercial vehicle leasing, lenders typically focus on:

- Consistent revenue and cash flow

- History of timely repayments

- Existing financial commitments

- Length of time trading

- Overall level of debt

- Stability of the business structure

Each lender will apply their own scoring model, meaning approval criteria can vary between providers.

We partner with the UK’s most reputable leasing and finance providers, giving us direct Tier One funder access and ensuring you have access to the best deals and flexible options available.

Some of the funders we work with include:

Do You Need Good Credit To Lease A Commercial Vehicle?

A strong credit profile will improve your chances of approval and provide access to more favourable commercial vehicle contract terms. Businesses with good credit are often offered:

- Lower monthly payments

- Reduced upfront deposits

- Greater vehicle choice

- More flexible contract options

That said, leasing is still possible with less-than-perfect credit. Some providers specialise in working with businesses that have weaker credit histories, although this may result in:

- Higher deposits

- Increased monthly payments

- More limited vehicle selection

- Stricter contract terms

Is There A Minimum Credit Score Required?

There is no universal minimum credit score for commercial vehicle leasing. Each finance provider uses its own internal criteria and scoring system.

As a general guideline, a stronger credit profile improves approval chances. However, lenders assess the full financial picture of your business rather than relying solely on a single number.

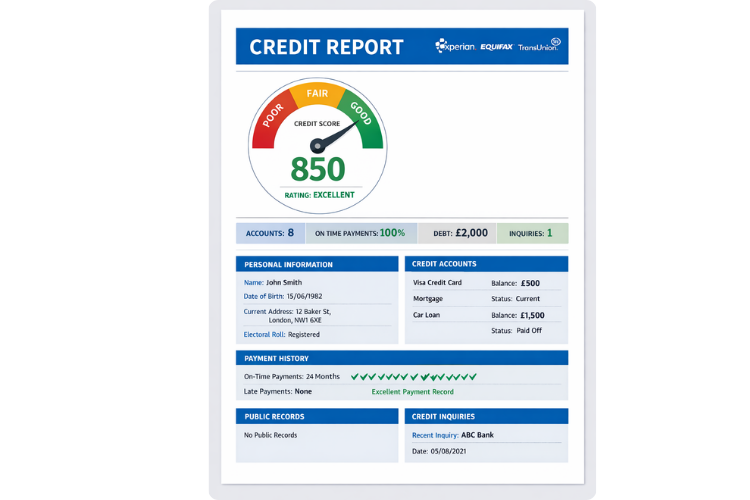

What Information Is Included In A Credit Report?

A typical credit report used in commercial vehicle finance may include:

- Business and/or personal identification details

- Trading and address history

- Credit accounts and repayment records

- Outstanding loans and credit facilities

- Public records such as CCJs or insolvency events

- Credit utilisation levels

- Recent credit applications

- Financial associations (e.g. linked accounts or directors)

Lenders use this information to evaluate affordability and risk before offering a commercial vehicle contract.

Can You Lease A Commercial Vehicle Without A Credit Check?

In most cases, no. Reputable finance providers are required to carry out affordability and credit assessments as part of responsible lending practices.

Offers that claim to provide “no credit check” leasing are uncommon and may come with significantly higher costs or alternative financing structures.

How Long Does A Decision Take?

Many applications receive an initial automated response within minutes. However, most commercial vehicle contract applications undergo manual review by an underwriter.

Typical timeframes:

- Instant or same-day initial decision

- 24–48 hours for full approval

- Up to several working days during busy periods

What Information Is Required To Apply?

When applying for a commercial vehicle lease, you’ll typically need to provide:

Business details:

- Company name and registration

- Trading address and history

- Nature of business activity

- Financial information (turnover, accounts, etc.)

Personal details (for directors/guarantors):

- Full name and date of birth

- Address history

- Contact information

- Financial details

Documentation may include:

- Proof of identity

- Proof of address

- Business bank statements

- Financial accounts or projections

- Driving licence

Improving Your Chances Of Approval

If you’re preparing to apply for a commercial vehicle contract, consider the following to strengthen your application:

- Maintain up-to-date and accurate financial records

- Reduce existing business debt where possible

- Ensure timely payments on current agreements

- Provide a higher initial deposit if feasible

- Keep business accounts healthy and well-documented

- Consider adding a guarantor if required

- Choose vehicles that align with your affordability

What Happens If Your Application Is Declined

If your application isn’t approved, it’s worth reviewing the possible reasons before reapplying. Common factors include:

- Limited trading history

- Poor or thin credit file

- Missed or late payments

- High levels of existing debt

- Incomplete or inaccurate application details

- Recent multiple credit applications

You can request feedback from the lender and review your credit profile to identify areas for improvement. Addressing any issues before reapplying can significantly increase your chances of success.

You can also check your eligibility for car leasing here

Find The Perfect Lease Deal Today!

With an impressive average score of 4.9 stars on Trustpilot, we believe our reviews reflect our commitment to customer service. Our knowledgeable team provides expert advice and guidance to help you choose the perfect vehicle and finance product for your needs.

With our extensive range of vehicles available for lease, you’re guaranteed to find the perfect vehicle to meet your needs. As proud members of the British Vehicle Rental and Leasing Association (BVRLA), we uphold the highest standards of service and professionalism. Plus, with our Price Promise, you can be confident you’re getting the best deal available. Rest assured, we are also authorised and regulated by the Financial Conduct Authority (FCA), ensuring transparency and trust in every transaction.

Many UK businesses have already benefited from our hassle-free approach to securing a brand-new vehicle, and now it’s your turn to take advantage of our exceptional services.

👉 Check our best van leasing deals now

Request your quick quote online today and explore our latest leasing deals.

Call our expert team on

Call our expert team on